Is Your Discretionary and Non-Discretionary Spending Plan Putting You in the Poor House?

What is Your Wealth Management Plan?

This will Help You in Your Wealth Management Plan to Embrace Wealth

Have you ever looked in the mirror and said to yourself…

“Wow, I thought I’d be further along by now.”

The truth is, if you haven’t been using proven systems for setting and achieving your life, financial, career, or business goals, then it’s not your fault!

Millions of people around the world are feeling lost, stuck, afraid of failure and not sure where to look…

And even more are stuck in a dead-end job, or seriously worried about their financial future.

That’s why I created this information. It’s a quick, easy to follow blog page to help you set, and achieve ANY Wealth Management Plan goal…

Even if you don’t know where to start, or are struggling to find your life’s purpose.

Here’s how it works.

Are You Giving Yourself Permission to be Prosperous, Abundant and Rich?

- What would you do with $10 million? (60 Seconds to Answer).

- What is your Hierarchy of values and financial destiny?

- What is financial wealth and authenticity to you?

- What is the value of wealth building to you?

- Are You Looking for The Breakthrough Experience?

Do You Need or Want Help With Any or All of the Following:

- Buying a car or a house, paying for a wedding, having kids, and other big expenses—stress free

- Using strategies to negotiate a big raise at work

- Set-it-and-forget-it Investment strategy that are simple and beat financial advisors at their own game

- Crush your debt and student loans faster than you thought possible

- Set up no-fee, high-interest bank accounts that won’t gouge you for every penny

- Automate your finances so your money goes exactly where you want it to—and how you can do it too

- Talk your way out of late fees (with word-for-word scripts)

- Save hundreds or even thousands per month (and still buy what you love)

- Choose the right accounts, small businesses or side business or investments so your money grows for you—automatically. Best of all, you spend guilt-free on the things you love.

- Or Other….

There is a change that is sweeping the world…

This change is silently transpiring in our midst and is more important than any which the world has ever undergone.

This change stands unparalleled in the history of the world.

You’ve seen newspapers or watched news broadcasts that proclaimed headlines like these.

“In the Midst of a Recession, This Company Posted Record Profits!”

“While Consumer Spending Is Down, Sales of Luxury Goods Are Up.”

“One Man’s Story of Unemployment and Bankruptcy to Million Dollar Success.”

“Even in an Downturn, This Business Keeps the Cash Register Cha-chinging!”

“Record Lay-offs, Record Unemployment, Record Foreclosures — and Record Bonuses!”

Sound familiar?

Of course they do. You’d have to be living underneath a rock not to have noticed what’s been happening all around us.

But what’s really happening?

- Why are some doing so well while others are … not?

- Why are so many struggling to make ends meet while others are living the high life?

- What’s really going on here?

What Do “These People” Financially Have That You Don’t? The Answer Will Surprise You…

The answer is …

Nothing.

They don’t have anything that you don’t have.

They just know and understand something that you don’t. Not yet, anyway…

Any Person Who Knows and Understands the Answer to This Question Has an Inconceivable Advantage over the People Around Them … One That Will Make Them Happier, Healthier, and Wealthier!

Personal finance teacher, mentor and coach Michael Kissinger asks you just five simple questions to get started with your Wealth Management Plan.

- Do You Know What You Are Truly Worth?

- Are you being paid that? Does it pay for all your bills and obligations?

- How have you applied that to your Wealth Management Plan?

- Do you earn enough under your Wealth Management Plan for you dreams ad goals? If not, answer:

- For $250,000+/- Annually Will You Build a Proven, High Profit, Low Overhead-Low Start Up, Risk Free, Guaranteed, Unlimited Income, Side Business?”

If yes, contact him now.

Michael has been called a “wealth planning wizard”. Now he’s updated and expanded his teaching, mentoring and money coaching for a new age, delivering a simple, powerful, no-BS 6-12 week program and Wealth Management Plan that just works. He Will Teach, Mentor and Coach You to Become Financially Free or Independent. See: Embracing Wealth – Giving Yourself Permission to be Fortunate | Dr John Demartini

What Do You Spend the Most Money On in Your Wealth Management Plan?

David Zimmerman on wrote and consumer spending is the fuel running the engine of the American economy. According to Investopedia, consumer spending accounts for a massive 70% of economic activity in the U.S. This means that trends in spending can exert a profound impact on the economic health of the United States as well as American businesses and households.

Americans opened their wallet to the tune of $14.5 trillion in purchases in just the first quarter of 2020. And this massive sum was spent at the start of a year that would ultimately be distinguished by a dramatic pandemic-related downturn in spending.

But where is all this money going, exactly? What do Americans spend the most on? From big-ticket items and long-term saving goals to daily living expenses and recreational experiences, where do Americans put their money? And how have these spending habits been impacted by the pandemic? The Secret Science Of Money

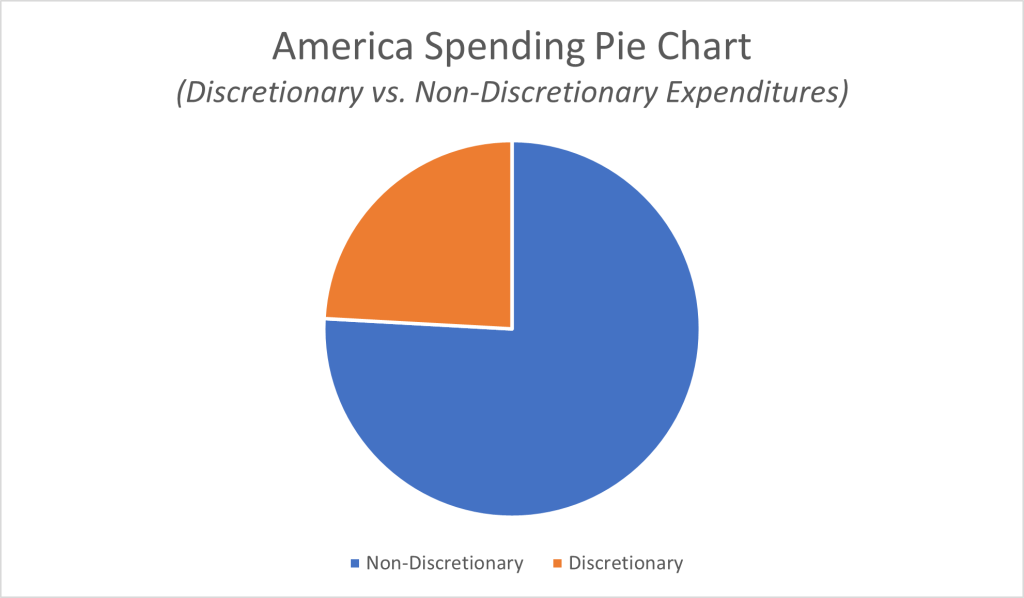

Discretionary and Non-Discretionary Consumer Spending in America

Before proceeding, we should note that consumer spending is typically divided into two broad categories—discretionary and non-discretionary spending.

Discretionary spending refers to non-essential expenses like home decor, entertainment, recreation, travel, and other items and services which are generally optional. Non-discretionary expense refers to consumer spending on necessary goods and services including housing, healthcare, food, clothing, and transportation.

Which expenses make up the largest slivers of the whole pie?

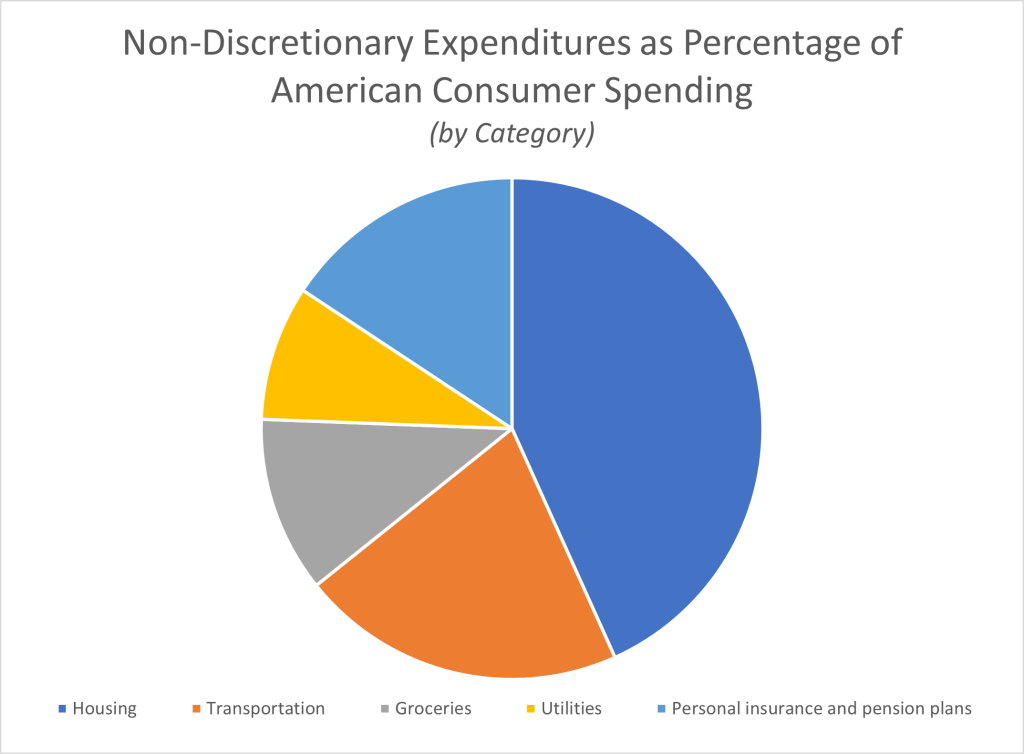

Non-Discretionary Expenses: Housing, Transportation, Healthcare, and More

Let’s first take a look at non-discretionary expenses, since these are the expenses for goods and services consumers have to have. How much does the average American spend on necessities?

The vast majority of Americans will dedicate well over 60% of their spending to non-discretionary expenses. As a result, it’s important to dive deeper into non-discretionary income spending habits—not just brush these off as unavoidable and unchangeable expenses—if we want to truly understand where and how Americans spend their money.

Most of the average household budget goes to needs, not wants. The figures below suggest that the high cost of living in the United States is a consequence of the burdensome costs imposed by the most consistent spending categories of non-discretionary expenses: housing, healthcare, and food.

What Is the Number 1 Expenditure for the US?

Shelter is a critical need for humans. You have to live somewhere, and for the average American—regardless of whether you rent, buy, or build a house—a place to live is the single largest expense. In fact, average Americans spend nearly a third of their total annual spending on a place they can call home.

According to a 2020 U.S. Bureau of Labor Statistics report on Consumer Expenditures (which references figures from 2018), the top expense among American consumers in either category of discretionary or nondiscretionary expenditures is housing. Rent and mortgage payments account for roughly 32.8% of all consumer spending. Also included in the housing expenditure category are the costs of property taxes, homeowners insurance, and repairs and maintenance.

This is a dominant expenditure for most Americans and (as a closer look below at housing markets in different major metropolitan areas demonstrates), the cost of shelter is a driving indicator of broader expenses in a given local market. Therefore, the cost of housing is often proportional to other costs in a given city, demonstrating the highly variable nature of consumer costs by region. We’ll explore this matter in more detail hereafter.

What Average Americans Spend on Other Categories of Non-Discretionary Expenses

Other major categories of American consumer spending include:

- Transportation: 15.9% of the average annual expenditure for American consumers

- Groceries: 8.6% of the average annual expenditure for American consumers

- Healthcare: 8.1% of the average annual expenditure for American consumers

- Utilities: 6.6% of the average annual expenditure for American consumers

Transportation

The big spending category of transportation expenditures includes car payments and expenses related to buying a car or vehicle, fueling, and maintaining a vehicle, as well as taking public transportation like buses, trains, and air travel, as well as other forms of transportation.

Groceries

If a recent grocery shopping trip has left you with a hefty bill to pay, it might not surprise you to find that food prepared or consumed at home is a major spending category for the average household in America. Fruits, vegetables, meat, eggs, dairy products, bakery products, cereals, and other staples are among the categories covered under the groceries, or food at home, category. Although shopping sales, using coupons, comparing prices and strategically using the best credit cards for buying groceries can all help cut down food costs and get consumers more for their money, food and groceries will continue to claim a solid chunk of consumers’ total average spend each year.

Health Care

Health care spending is another of the biggest expense categories for average Americans. In its definition of healthcare expenditures, the BLS includes consumer spending on health insurance premiums, health care and medical services, medical equipment and prescription and over-the-counter medications, vitamins, and supplements.

Utilities

Spending on utilities, fuels, and public services encompasses spending on electricity, natural gas and other fuel sources, water, sewage maintenance, telephone charges, and trash collection services. Depending on their area of service, consumers may or may not have the opportunity to shop around for providers. However, they can take other steps to save on utilities, often by using more efficient equipment or otherwise reducing usage.

Personal Insurance and Pensions

In addition to these expenses, the Consumer Expenditures report notes that spending on Personal Insurance and Pension plans came in at 11.9% of spending in 2018. Personal insurance expenses include premium costs for all sorts of personal insurance coverage, including life insurance, disability insurance, mortgage insurance, accident insurance, personal liability insurance, and car insurance. In this category, you will also find contributions to retirement savings plans through Social Security, employer- and government-provided pensions or retirement plans, and IRA retirement plans for self-employed workers.

Discretionary Expenses in Your Wealth Management Plan

Now that we’ve seen how much the average American spent on the things they need, let’s look at how Americans spend their money on the things they want.

What Are Discretionary Expenditures?

This category of discretionary expenditures refers to elective spending on non-essential goods, services, and experiences. While these spending categories form a much smaller piece of the spending pie for most Americans, taken together, they constitute around a quarter of all spending per year. The figures below are also drawn from the 2020 U.S. BLS report on Consumer Expenditures, and provide a breakdown of the top goods and services accounting for discretionary household spending in 2018.

The Biggest Spending Categories in Discretionary Purchases

Two spending categories led discretionary income spending in 2018, both coming in at 5.6% of the average household budget: dining out and entertainment.

Dining out includes spending at restaurants (and tipping your server), convenience stores, vending machines, and more.

According to Investopedia, the Entertainment spending category includes spending on things like sporting goods, bikes, hunting and fishing supplies, and other recreational equipment.

Additional discretionary expenses include:

- Gifts: 2.2%

- Consumer Electronics: 2%

- Alcohol and Tobacco: 1.6%

- Travel Lodging: 1.4%

- Toys and Hobbies: 1.4%

- Tickets: 1.3%

- Apparel Products and Services: 3%

Some of these spending categories could benefit from some further clarification. For instance, “Tickets” refers to spending on event attendance including sporting events, concerts, movie theaters, stage productions, wrestling tournaments, and more. The category identified as “Toys and Hobbies” also includes playground equipment and pet supplies. As to the last of these, pet food and veterinary care actually account for the biggest proportion of the 1.4% itemized above. The category of “Apparel Products and Services” includes expenses such as dry cleaning, clothing storage, jewelry and watch repair, tailoring, rental and more.

As the bulleted list above demonstrates, these expenses generally extend from the lifestyle priorities of American consumers. Evidence suggests that a big source of fuel for the American economic engine is channeled through recreational activities that include the pursuit of entertainment, event attendance, vacations, physical activeness, hobbyist activities, and of course, our pets.

Spending Preferences in Major Cities

The figures above offer a look, by percentage, at all the things Americans work into their budget both out of necessity and desire. But these percentages only tell a part of the story. As noted at the outset, there are dramatic differences in the cost of living from one region to the next, and even between two cities in the same state.

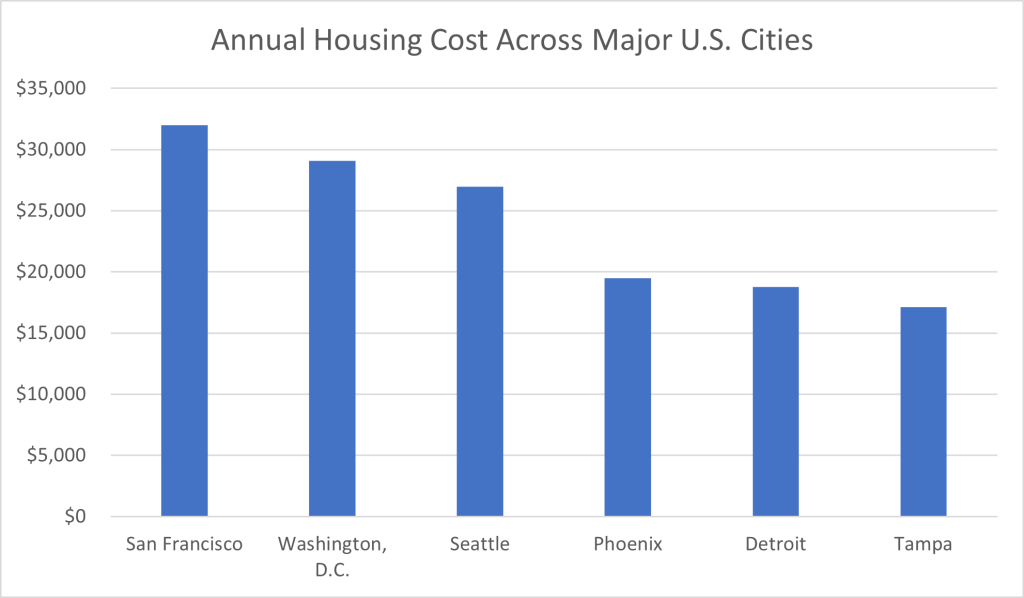

How Housing Costs Compare Across Major U.S. Cities

To this point, Insider reports on “Bureau of Labor Statistics’ Consumer Expenditure Surveys per city. The data covers the most recent period of 2016 to 2017 and reveals average annual expenditures for consumer units 22 major metros in the Northeast, South, West, and Midwest.” The findings show that the costs for food, housing and transportation (the “Big Three” American expenses) for 22 major cities demonstrate certain parallels but also show that the biggest difference in consumer spending from one major metropolitan area to the next largely comes down to the cost of housing.

For instance, this cost is as high as $26,965 per year in Seattle, $29,101 per year in Washington D.C. and, at the top of the pack, San Francisco, where the average resident pays in excess of $32,000 for housing per year. This contrasts the cost for housing in major cities like Phoenix ($19,491 per year), Detroit ($18,794 per year) and Tampa ($17,131 per year). In other words, the cost of housing in Washington DC is nearly twice what you might spend for a similar space in Tampa.

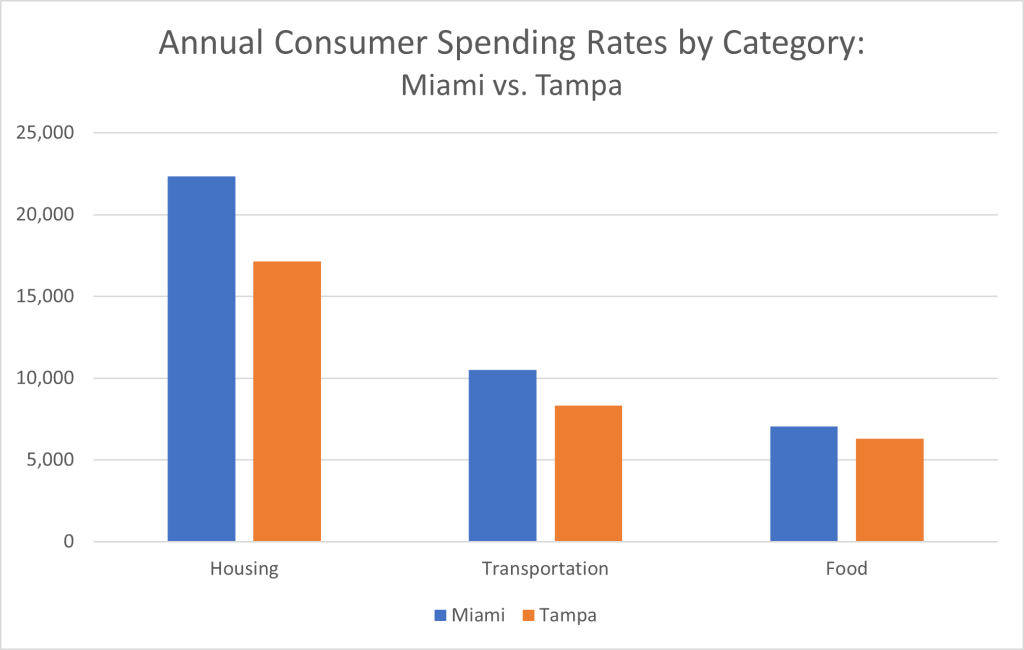

Speaking of Tampa, this South Florida city is roughly 280 miles away from another South Florida Metro area—Miami. According to Insider, housing in Miami notched a mark of $22,350 per year, denoting a more than 20% premium on the cost of living relative to Tampa. Similar proportions separate the two cities over the cost of transportation ($10,507 vs. $8,307 in Tampa), whereas the difference in the cost of food ($7,040 in Miami vs. $6,289 in Tampa) is less extreme.

Evidence suggests that food costs are often fairly comparable from one major city to the next, whereas transportation is highly variable. It is entirely possible that this variation has more to do with how effectively each city has invested in public and mass transit than with the scale of economy in a given city. In other words, the cost of housing would appear to be a far better indicator of the economic scale in each major metropolitan area.

The Connection Between Job Opportunities and Housing Costs

The highest ranking cities on this list in terms of housing cost are also generally those with the most robust local economies, the highest salary ranges for local workers, and the widest range of gainful employment opportunities. Such is to say that the cost of housing in a city may be a strong indicator of what consumers are willing and able to spend to live in more desirable metro areas.

COVID-19 and American Spending Habits 2020

Bear in mind that the data highlighted above—both in terms of percentage of spending in different areas, and in terms of cost per city—all predate the COVID-19 pandemic. Dramatic shifts in spending during the last two years have altered the short-term landscape for consumer spending. However, it isn’t clear that any of these changes will constitute long-term shifts in how Americans spend their money. That is an assessment that we can only make with the benefit of several more years hindsight. Until then, we can only evaluate the direct and immediate impact made by the pandemic on consumer spending habits.

To this end, the Bureau of Labor Statistics provided a New Release from September of 2021 highlighting some of the most readily observable changes in consumer spending following the emergence of the pandemic and its manifold impacts on businesses, consumers, and lifestyle choices throughout 2020.

Evidence suggests the biggest impact on consumer spending was felt in specific areas of discretionary income spending connected to recreation and entertainment outside of the home. Here, the BLS points to the direct shifts in consumer spending between 2019 and 2020 “for all units.” Units are “classified by income before taxes by quintile, decile, and range; age of the reference person; size of the consumer unit; composition of the consumer unit; number of earners; housing tenure (homeowner or renter) and type of area (urban or rural); region of residence; occupation; highest education level of any consumer unit member; race; Hispanic or Latino origin; and generation of the reference person.”

Across all units, reports the BLS, consumer spending in 2020 came in at $61,334. This denotes a 2.7% decrease from the prior year. This decline in spending wasn’t simply an across-the-board decline. To the contrary, it reflected declines in certain areas specifically connected to business closures, lockdowns, and quarantines as a consequence of the pandemic.

For instance, spending on apparel and related services was down a staggering 23.8% over a single year, especially among men and boys. This was driven by a sharp downturn in brick-and-mortar shopping for items like footwear and sports apparel. For further confirmation that consumer spending in select areas was crippled by the pandemic, note that while retail alcohol sales for in-home consumption rose by 4.5%, spending on alcoholic beverages outside of the home was down a dramatic 43.9%

Also down, says the BLS, was spending on food outside of the home, which declined by 32.6%; transportation, which saw an especially sharp drop off of 66.3% in the area of public transportation alongside a 25.1% fall in spending on fuel; and entertainment outside of the home, which saw ticket and admissions sales fall by a devastating 51.7%.

Areas that saw increases in consumer spending include mortgages and expenditures relating to home ownership, the latter of which spiked by 9.9% on the strength of various elective home renovation projects; cash contributions such as child support payments, contributions to religious groups, charitable donations, or political funding, which collectively jumped by 14.4%; and spending on in-home entertainment options including hobbies and toys (up 21.4%) and entertainment equipment (up 48.8%).

The takeaway from these BLS figures is that consumer spending generally declined, but more importantly, the focus of discretionary consumer spending shifted to a greater emphasis on in-home items and experiences. As a result, the sharpest declines were felt in the sectors catering most to out-of-house experiences. At the same time, some of this economic impact was offset by added spending for in-home expenses.

Post-Lockdown Consumer Spending

While 2020 saw shifts in consumer spending habits, there is no evidence to suggest that these changes will be permanent. Once again, only the next several years will tell us the precise trajectory of consumer spending habits. However, we have sufficient proof in just the last year that certain spending habits will likely return to pre-2020 levels as more time passes following the first phase of the pandemic.

The subsequent phase of the pandemic has been marked by the widespread proliferation of COVID-19 vaccines alongside an array of public health and safety strategies aimed at management of viral spread, in lieu of lockdowns and shutdowns. These steps have resulted in a broad-based reopening of the economy—and in particular, of recreational and consumer opportunities outside of the home.

American Spending Habits 2021

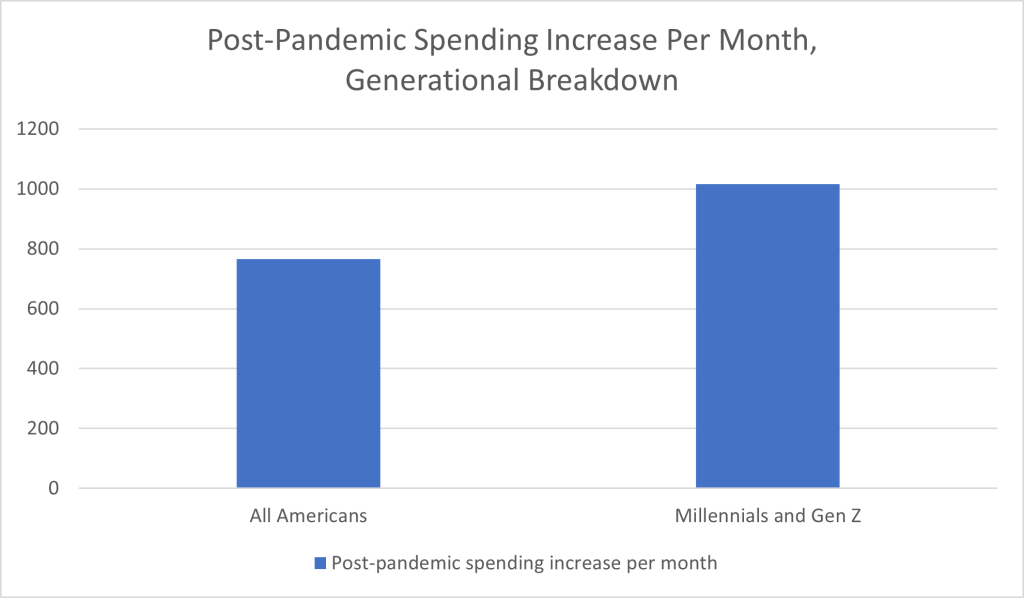

With restaurants reopening, bands going back on tour, Broadway shows resuming their runs, theaters once again screening films, and sports teams inviting fans back into their stadiums, 2021 is seeing a major rebound of outbound consumer spending. CNBC reports that “Between dining out and taking trips, Americans are now spending an average of $765 more a month compared with last year when much of the country was shut down due to the coronavirus pandemic, according to the MassMutual Consumer Spending & Saving Index.”

Spending habits vary depending on several factors, with age and income level being among the most important. This pattern holds true for post-pandemic economic recovery, as well.

Younger age groups, in particular, seem determined to return the American consumer economy to its former heights of glory, spending on recreational opportunities outside of the home with a newfound ferocity, according to CNBC. Millennials and Gen Z, apparently making up for time lost during the pandemic, were spending $1,016 more per month in the summer of 2021 as compared to the prior year.

And yet, even in the face of these promising figures, new variants of the COVID-19 virus—like Delta and Omicron—have already left their mark on consumer spending. As with the pandemic in general, there remains so much about consumer spending in this era that remains uncertain. How we weather the next several stages of life in the COVID era will likely have a direct bearing on how and where Americans spend their money.

American Spending Habits 2022 Update

Like the years that preceded it, 2022 brought plenty of stress and challenges for consumers. Pandemic-related lockdowns were over, but high inflation rates—and high costs in general across major spending categories—characterized the economy.

McKinsey & Company reported in May that 2022 consumer spending habits thus far had represented both a departure from pandemic restrictions and longer-term adaptations to Covid-era practices—for example, after years of lockdowns and social distancing, consumers were starting to make their way back to in-person shopping but still relied heavily on online shopping.

In June, Forbes forecasted that Americans would “keep spending in 2022” and into 2023, with consumer spending cutbacks predicted to fall closer to 2024. An August 2022 NPR article on inflation noted not only consumers’ spending concerns but also businesses’ efforts to offer affordable options despite the rising inflation rate.

Deloitte’s State of the Consumer Tracker reported in November that concerns over high costs, rising inflation, and personal savings levels had led to three consecutive months of Americans planning to spend less money in the coming month.

Create Your Personal Wealth Management Plan Today

Wealth Management Plan Assessments

Are you Exceeding these Average Annual Expenditure for Your Expenditures?

What Are Your Non-discretionary Expenses? They refers to consumer spending on necessary goods and services including housing, healthcare, food, clothing, and transportation. Calculate what you are spending on Non-Discretionary Expenses. What is your current income? Now allocate your acceptable spending limits! Have you exceeded the average expenditures? Why? What do you need to do to reach the acceptable levels?

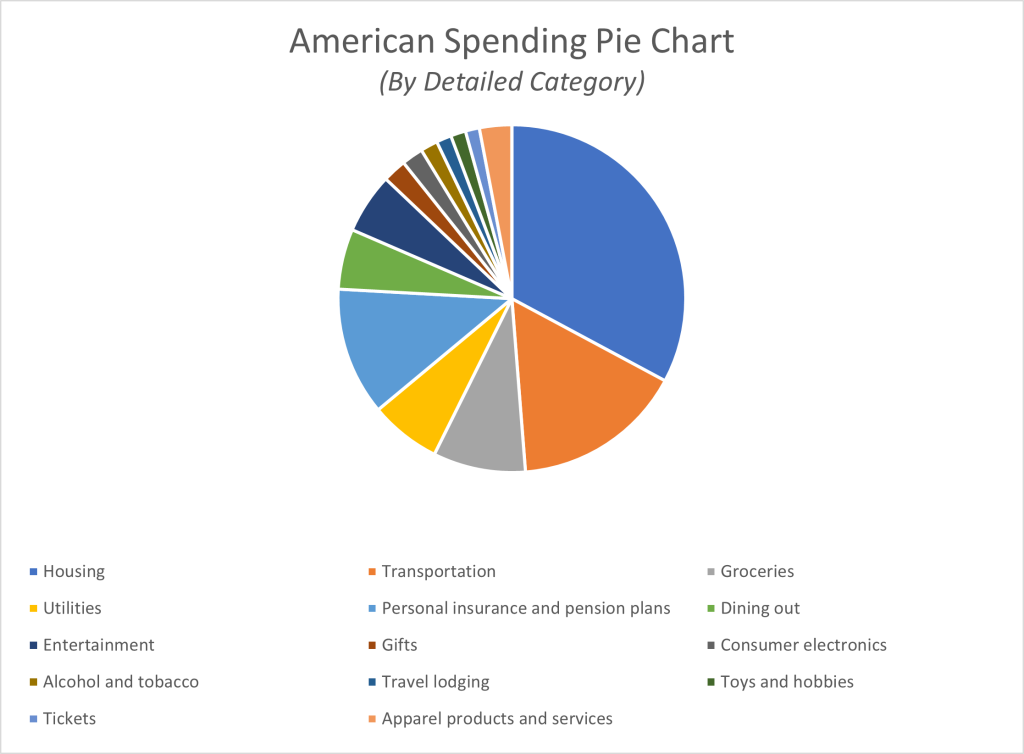

- Housing: 32.8% of the average annual expenditure for American consumers Also included in the housing expenditure category are the costs of property taxes, homeowners insurance, and repairs and maintenance.

- Healthcare: 8.1% of the average annual expenditure for American consumers

- Transportation: 15.9% of the average annual expenditure for American consumers

- Groceries: 8.6% of the average annual expenditure for American consumers

- Utilities: 6.6% of the average annual expenditure for American consumers

What Are Your Discretionary Spending Expenses. They refers to non-essential expenses like home decor, entertainment, recreation, travel, and other items and services which are generally optional. Calculate what you are spending on Non-Discretionary Expenses. What is your current income? Now allocate your acceptable spending limits! Have you exceeded the average expenditures? Why? What do you need to do to reach the acceptable levels?

- Dining out: 2.3%

- Entertainment: 2.3%

- Gifts: 2.2%

- Consumer Electronics: 2%

- Alcohol and Tobacco: 1.6%

- Travel Lodging: 1.4%

- Toys and Hobbies: 1.4%

- Tickets: 1.3%

- Apparel Products and Services: 3%

Coaching for Your Wealth Management and Planning

[1]: The Power of Financial Education Coaching – An Unfair Advantage

In this coaching we take a new and hard-hitting look at the factors that impact people from all walks of life as they struggle to cope with change and challenges that impact their financial world.

In this coaching we underscore our messages and challenge you to change your context and act in a new way. You are advised to stop blindly accepting that you are ‘disadvantaged’ with limited options. You are encouraged to act beyond you concept of limited options and challenge the preconception that you will struggle financially all of you life.

This contact includes clear, actionable steps that any individual or family can take, starting with education. Education becomes applied knowledge, a powerful tactic with measurable results.

You will be challenged to understand two points of view, and experience how financial knowledge is your unfair advantage.

Why the rich get richer even in a financial crisis?

In this coaching, we confirm our message and challenge you to change your context and act in a new way. You are advised to stop blindly accepting that you are ‘disadvantaged’ with limited options and challenge the notion that you will struggle, financially, all your life.

What does school teach you about money?

In most cases, the answer is “Not much.” If there is any financial education, the courses are taught by financial planners and bankers… the agents of Wall Street and the big banks, the very people that caused and profited from the financial crisis.

This coaching is about real financial education. It is about how debt and taxes make the rich richer and why debt and taxes makes the poor and middle class struggle. Financial Education Video – The Secret To Getting Rich With Nothing | Robert Kiyosaki Interview 2023

This coaching explains why the rich get richer, paying less in taxes, while the middle class shrinks with many losing jobs, homes, and retirement and paying more in taxes. This coaching is about the five unfair advantages a real financial education offers.

- The Unfair Advantage of Knowledge

- The Unfair Advantage of Taxes

- The Unfair Advantage of Debt

- The Unfair Advantage of Risk

- The Unfair Advantage of Compensation

- These five unfair advantages are the outcomes of real financial education. Unfair Advantage-The Power of Financial Education

[2]: Financial IQ Improvement Coaching

We firmly believed that the best investment one can ever make is in taking the time to truly understand how one’s finances work. Too many people are much more interested in the quick-hitting scheme, or trying to find a short-cut to real wealth. We have preached over and over again, one has to truly under the process of how money works before one can start out on trying to escape the daily financial Rat Race.

In this coaching we lay out 5 key principles of Financial Intelligence for all to understand. In INCREASE YOUR FINANCIAL IQ, we provide real insights on these key steps to wealth:

- How to increase your money — how to assess what you’re really worth now, what your prospects are, and how to start mapping out your financial future.

- How to protect your money — for better or for worse, taxes are a way of life. Kiyosaki shows you that “it’s not what you make….it’s what you keep.”

- How to budget your money — everybody wants to live large, but you have to learn how to live within your budget. Kiyosaki shows you how you can.

- How to leverage your money — as you build your financial IQ, knowing how to put your money to work for you is a crucial step.

- How to improve your financial information — We show you how to accelerate your wealth as you learn more and more. Increase your financial IQ

[3]: Cashflow Quadrant Coaching

CASHFLOW Quadrant Coaching is a guide to financial freedom. It reveals how some people work less, earn more, pay less in taxes, and learn to become financially free.

It for those who are ready to move beyond job security and enter the world of financial freedom. It’s for those who want to make significant changes in their lives and take control of their financial future.

We believe that the reason most people struggle financially is because they’ve spent years in school but were never taught about money. We teach and coach that this lack of financial education is why so many people work so hard all their lives for money…instead of learning how to make money work for them.

This teaching, mentor and coaching will change the way you think about jobs, careers, and owning your own business and inspire you to learn the rules of money that the rich use to build and grow their wealth. .Cashflow Quadrant Guide to Financial Management and Freedom

Follow a personal financial development plan for wealth and your personal life or use a template to start accomplishing your goals and improving your life.

For the easiest way to get started, download my free Personal Development Plan Template to organize your goals over the next few months and years and optimize your success.

[4]: Business of the 21st Century Coaching

This mentoring and coaching explains the revolutionary business of network marketing in context of what makes any business a success in any economic situation. This coaching and book lends credibility to the Networking business, and justifies why it is an ideal avenue to make money. The Business of the 21st Century.

[5]: Tax Secrets for Entrepreneurs Coaching

Do you look at your paycheck every month and shudder at the amount of money that’s taken from you in taxes? What about the amount you have to pay at the end of each fiscal year?

It’s been said that taxes are one of the certainties in life; something we all have to deal with. Though this may be true, taxes don’t have to be the burden they currently are. There are ways taxes can actually be beneficial.

We are dedicated to helping the average person use the same financial knowledge and strategies that the rich have traditionally kept to themselves. In our Tax Secrets coaching we will introduce you to multiple ways the tax code can actually help you build wealth and keep more of your hard-earned money.

If you’re sick of seeing so much of your money swallowed up by taxes each year, let us coach you on Tax Secrets. You’ll learn what you can do to change your tax challenges. Tax Secrets for Entrepreneurs

How the Rich Use Debt and Taxes to Get Richer – Robert Kiyosaki

[6]: What the Rich Invest in the Poor and Middle Class Do Not Coaching

Investing means different things to different people… and there is a huge difference between passive investing and becoming an active, engaged investor. This coaching covers the basic rules of investing, how to reduce your investment risk, how to convert your earned income into passive income… plus the 10 Investor Controls.

This coaching makes a key distinction between managing your money and growing it… Understanding key principles of investing is the first step toward creating and growing wealth. This coaching delivers guidance, not guarantees, to help anyone begin the process of becoming an active investor on the road to financial freedom. Guide To Investing

[7]: Retire Young – Retire Rich Coaching

If you don’t plan on working hard all your life… this coaching is for you. If you’re ready to retire (or want to retire early enough to enjoy your retirement years) you can learn how to started with nothing and “retired” – financially free – in 5 years and less than 10 years. This coaching makes the case for how a context shift in the way we think about money and investing allows us to see opportunities others miss and create the life you deserve. RETIRE YOUNG RETIRE RICH FULL

[8]: Think and Grow Coaching

What Is Think and Grow Rich About?

Think and Grow Rich is the combined wisdom from more than 500 of America’s most successful individuals. Their insights were then narrowed down into 13 principles and contribute to what Hill refers to as an overall “Philosophy of Achievement.” However, refusing to let Think and Grow Rich be defined purely as a method or system for success, Hill stated that the goals of his book were:

- To help you become self-aware. Think and Grow Rich Workbook

- To help you understand how to become more effective amidst the immutable laws of the universe. Self Analysis Questions from Think and Grow Rich by Napoleon Hill

What Are the 13 Principles of Think and Grow Rich?

Napoleon Hill’s 13 principles of success present a philosophy of achievement that is intended to be mulled over. This Think and Grow Rich summary will look at each of the 13 principles in turn. They are as follows:

- Desire

- Faith

- Auto-suggestion

- Specialized Knowledge

- Imagination

- Organized Planning

- Decision

- Persistence

- The Power of the Master Mind

- Sex Transmutation

- The Subconscious Mind

- The Brain

- The Sixth Sense

- Uniquely philosophical and, at times, veering on spiritual, Think and Grow Rich has become a seminal book for entrepreneurs, CEOs, and individual thinkers alike. By reading the key points from this Think and Grow Rich chapter summary, you’ll learn how to master your subconscious and command your destiny. Think And Grow Rich By Napoleon Hill)

How to Get Abundant or Prosperous or Rich

The Starting Point of All Achievement Personal Development Coaching and Mentoring

The key to all success is to define a goal and to pour all of your energy, power, and effort into achieving it. It may take many years before you are successful, but if you hold onto your desire, you will eventually attain what you seek.

Merely wishing for money will get you nowhere. However, to desire riches by way of an obsessive goal, a meticulous plan, and not accepting failure as an option, you’ll become rich. The Master Key System by Charles F. Haanel To help you do so, we start your coaching on the the MKS Master Key System and Think and Grow Rich Six Steps:

- Decide exactly how much money you wish to make, to the dollar.

- Determine what you are willing to give to receive this amount of money.

- Choose a date by which you want to have amassed this amount of money.

- Create a plan of how to achieve your goal and begin at once, whether you feel ready or not.

- Write all of the above down in a clear statement.

- Read this written statement aloud, twice a day – first thing in the morning and last thing at night. Visualize your life as if you already own this amount of money.

While being able to visualize yourself as rich may seem challenging at first, it’s only those individuals who are “money conscious” that become successful. To be money conscious is to see yourself in possession of great wealth before you attain it. You will only become rich if you possess a deep desire for money, and you stop at nothing to get it. TThe Universal Laws

Apply the Shoaff Red Cadillac Convertible Philosophy To Get What You Want

There is an infinite abundance in this universe. Not only is there an infinite abundance of happiness, faith, love, courage, joy, humility, wisdom, generosity, peace, gentleness, meekness, patience, kindness, and all such qualities one could ever desire to express habitually, but there is an infinite abundance of every material thing that one could ever desire to have in order to express his individuality.

So, the reason that so many people do not have the above in abundance is not because there is any shortage, it is simply because they are not aware of how to push the right button of appropriation.

All things that one desires are available to one who understands the “Laws of Appropriation.”

In other words, there is a simple set of rules by which all things are obtained, which anyone who really wants to learn them can learn and then be whatever he wants to be and have whatever he wants to have.

If you will learn the ideas contained in this message and use it, we guarantee that you will realize your most cherished dreams.

John Earl Shoaff was an American entrepreneur and motivational speaker. Shoaff was President and Board Chairman of the Nutri-Bio Corporation, an organization which sold vitamin, mineral, and protein dietary food supplements.

Shoaff was influential in the early career of Jim Rohn who left an estate of over $500 million, another American entrepreneur, motivational speaker and writer.

“How To Become A Millionaire” Coaching

Universal Law and Mind Programs Coaching

Program 1. See: “The Man in the Glass”

Program 2. See: The Gal in the Glass | Mindset Growth for Entrepreneurs

Program 3. See: The 7-Day Mental Diet – How To Change Your Life In A Week by Emmet Fox

Program 4. See: The Ten Laws Of Abundance

Program 5. See: The Science of Getting Rich By Wallace Wattles

Program 6. See: Entering The Large Sums Of Money Mindset

Program 7. See: Guided Meditation Large Sums Of Money Come To Me Easily And Quickly

EARL SHOAFF COACHING

Program 1. How to become a millionaire ~ Earl Shoaff See: How to become a millionaire ~ Earl Shoaff

Program 2. Earl Shoaff – 16 Lessons On How To Get What You Want (963hz) See: Earl Shoaff – 16 Lessons On How To Get What You Want (963hz)

Program 3. Earl Shoaff – How To Properly Plant Your Seeds See: Earl Shoaff – How To Properly Plant Your Seeds

STUART WILD, DR. JOSEPH MURPHY, CATHERINE PONDER and BRIAN SCOTT COACHING

Program 1. The Ten Laws Of Abundance See: The Ten Laws Of Abundance

Program 2. How To Attract Money By Dr. Joseph Murphy See: How To Attract Money By Dr. Joseph Murphy

Program 3. Financial Independence Can Be Yours See: Catherine Ponder – Financial Independence Can Be Yours

Program 4. The Dynamic Laws of Prosperity See: The Dynamic Laws of Prosperity by Catherine Ponder

Program 5. The Integral Laws Of Prosperity See: The Integral Laws Of Prosperity

Program 6. Wells Of Abundance 7 Planes Of Supply And The Law Of Increase See; Wells Of Abundance 7 Planes Of Supply And The Law Of Increase

JIM ROHN COACHING

Program 1. The Art Of EXCEPTIONAL Living By Jim Rohn: See: The Art Of EXCEPTIONAL Living By Jim Rohn.

Program 2. How to Take Charge of Your Life – Jim Rohn Multi-millionaire See: How to Take Charge of Your Life – Jim Rohn Personal Development

Program 3. How to Have the Best Year Ever! – Personal Development Life Coaching by Jim Rohn See: How to Have the Best Year Ever!

Program 4. Seven Strategies for Wealth & Happiness by Jim Rohn: See: 7 Strategies for Wealth & Happiness with Jim Rohn

Program 5. Five Major Pieces to the Life Puzzle Masterclass by Jim Rohn: See: Jim Rohn- Five Major Pieces to the Life Puzzle Masterclass

Program 6. The Richest Man in Babylon by George Clayson: See: The Richest Man in Babylon https://www.youtube.com/watch?v=wglndSWrvsM&t=33s

Program 7. the Books that Earl Shoaff Recommended: Shares the Books that his Mentor Earl Shoaff Recommended – Jim Rohn

DR JOHN DEMARTINI COACHING

Program 1. Seven Areas of Life to Empower: See: 7 Areas of Life to Empower | Dr John Demartini

Need Coaching Help with Your Wealth Management Success?

Making seemingly impossible things happen in any area of your life or business is our specialty, and we have a proven process that goes against much of what you’ve learned about manifestation and goal achievement in the past.

NINE TAKE AWAYS

The majority of people (even the “educated”) experience financial problems because they have not learned how the rich acquired their wealth and continue to make it grow.

In this coaching we share how we learned the 9 lessons of wealth from our mentors and coaches. We then offer to share this knowledge with you so you become financially free. When you complete this coaching you will learn, understand and apply the NINE TAKE AWAYS .

TAKE AWAY 1: The Rich Don’t Work for Money

TAKE AWAY 2: The Rich Learn How Money Works

TAKE AWAY 3: The Rich Mind Their Own Business (Assets)

TAKE AWAY 4: The Rich Use Corporations

TAKE AWAY 5: The Rich Have High Financial IQ

TAKE AWAY 6: The Rich Work to Learn

TAKE AWAY 7: The Rich Train Their Mindset

TAKE AWAY 8: 10 Steps to Get Started

TAKE AWAY 9: Our Coaching Process for Continual Growth

Over 25,000 achievers have now used MKS Master Key Coaching and Systems, the world’s #1 systems, for self or business or financial improvement. We’re grateful for this year and opportunity to serve you.

Please enjoy the above programs! Remember: You Are Greater Than You Think Wishing you and yours a wonderful New Year!

Let’s make the year extraordinary, together as you study The Science of Getting Rich

Cheering you on, always!

Join a “Year of MKS Master Key Mastery Coaching Programs and Systems”. We’ll spend the first Mondays of the Week with you taking you through advanced personal growth, business growth, profitability optimization and productivity so you can win this year and every years you are in business.

These are just a few tips to look out for when considering Breaking Through Your Upper Limits.

We personally believe this is the best way forward if you are looking for a Breaking Through Your Upper Limits. This is for people who have a dream or desire to be financially independent and are willing to put in the hard work to do so.

Wishing you prosperity and success. Remember You Were Born Rich

Michael Kissinger and Sydney Reitenbach

Phone: 650-515-7545

LinkedIn Profile: https://www.linkedin.com/in/michael-kissinger-a66b214/

E-mail: mjkkissinger@yahoo.com

Facebook: https://www.facebook.com/michael.kissinger.35

CONTACT US: [LIFE SUCCESS ASSESSMENT] [READINESS ASSESSMENT] [SERVICES] [ABOUT COACHES] [FAQs] [FEE RANGE] [COACHING AGREEMENT] [SURVEY] [PRESS RELEASE] Home

Web: https://mksmasterkeycoaching.com

Terms of Use | Testimonials and Results Disclosure | Privacy Policy

© Copyright 2023 –Reitenbach-Kissinger Success Institute – All Rights

Disclaimer

The Reitenbach-Kissinger Success Institute makes no guarantee, makes no promises regarding the outcome of using any of the information on this site or its product or service. The Reitenbach-Kissinger Success Institute is not liable for any damages arising in contract, tort or other wise from the use of or inability to use this site or any material contained in it, or from any action or decision taken as a result of using this site or the information hereon. The information on this site is informational only

The materials on this site comprise the The Reitenbach-Kissinger Success Institute views; they do not constitute legal or other professional advise or guarantee of any kind. You should consult your professional advisor for legal or other advice.

This site offers links to other sites thereby enabling you to leave this site and go directly to the linked site. The The Reitenbach-Kissinger Success Institute is not responsible for their content of any linked site or any link in a linked site. The The Reitenbach-Kissinger Success Institute is not responsible for any transmission received from any linked site. the links are provided to assist visitors to the Reitenbach-Kissinger Success Institute site and the inclusion of a link does not imply that the The Reitenbach-Kissinger Success Institute endorses or has approved the linked site